- The Value Mindset

- Posts

- Live Like Yesterday, Invest For Tomorrow: The Time-Shifted Wealth Strategy

Live Like Yesterday, Invest For Tomorrow: The Time-Shifted Wealth Strategy

Alex Kirkendall

March 09, 2025

Who this is for: Young to mid-career professionals with steady income growth who want financial freedom without feeling deprived along the way.

Key Takeaways:

Live on what you earned 5-10 years ago, not what you earn today

Invest the difference between your current salary and your "time-shifted" lifestyle

Gradually increase the time gap as you age for a smooth transition to retirement

We've all nodded along to the standard financial advice: "Housing should be 30% of your income," "Save 15% for retirement," and so on. But what if you could follow these same guidelines while supercharging your wealth-building? That's exactly what the Time-Shifted Wealth Strategy offers.

I'm not here to overturn conventional wisdom. I'm showing you how to reframe it for dramatically better results.

The Concept: Time-Shifted Lifestyle

Here's the fundamental idea: Always live as if you're earning what you made 5-10 years ago.

Think of it as intentionally creating a time lag between your earning power and your spending habits. Your lifestyle improves consistently—just on a delay.

For a college grad starting at $60K who sees steady 5% annual increases, this means that by year six, you're earning $76,576 but living as if you're making $60,000. The beauty? You're still following all those traditional percentage-based rules—just applied to a previous salary.

Starting Out: The Foundation Years

Let's get specific about those crucial first five years after college.

When you land that first $60K job at 22, you don't have a "5 years ago" reference point. So instead, embrace what I call the "foundation phase":

Live as lean as reasonably possible without being miserable. That means:

Having roommates or creative living strategies might be smarter than traditional living or home purchase

That 2015 Honda is perfectly fine (the 2025 model can wait)

Cooking at home most nights while treating the occasional restaurant visit as exactly that—a treat

While your college friends are rushing to fill new apartments with Wayfair furniture and maxing out their financial planner "approved" housing budget, you're building an investment advantage they can't catch.

The Magic Starts in Year Six

By year six, earning $76,576, conventional wisdom says you "deserve" to spend more. And guess what? You will spend more—just based on your $60K reference point, not your current salary.

Let's break it down:

Housing: 30% of $60K = $18,000/year ($1,500/month)

Transportation: 15% of $60K = $9,000/year

Food/Groceries: 12% of $60K = $7,200/year

Meanwhile, your investments include:

Standard 15% of your reference salary: $9,000

PLUS the entire salary gap: $16,576

That's $25,576 invested annually—without feeling any more deprived than the responsible version of your younger self.

I would like to clarify one point – I don’t agree with having set percentages of your salary to “target” for different categories of your life – I will breakdown a much better method in a future article. I do, however, concede to the fact that:

1) It’s commonly established in the financial planning industry

2) Can provide a meaningful baseline/proxy for comparing your current situation too

Stretching the Lag As You Age

As your career progresses, the strategy evolves:

Early 30s: Push to living 6-7 years behind

Late 30s/Early 40s: Stretch to 8 years behind

Mid-40s onward: Aim for the full 10 years behind

By your mid-40s, you might be making $150K but living on what you earned at 35 (perhaps $95K). That's still a very comfortable lifestyle—significantly better than your 20s—while investing at levels most people find impossible.

What This Looks Like in Real Life

This isn't about extreme frugality. Let me illustrate:

At 45, earning $150K, your friend buys a $45,000 car (30% of annual income on transportation). You, following the time-shifted strategy, buy a $28,500 car (30% of your 10-years-ago $95K salary).

You're still driving a very nice vehicle—just not the absolute top-of-line model your current salary could technically "justify."

The same applies to housing, vacations, and other expenses. You're not going without—you're just calibrating to a different reference point.

The Retirement Transition Nobody Talks About

Here's where this approach truly shines. Most financial planning ignores a critical psychological reality: downgrading your lifestyle feels terrible.

If you've spent decades living at the very edge of your income, any reduction in retirement hits hard. But if you're already living on what you made 10 years ago, you've built in a buffer that makes the retirement transition nearly seamless.

Who This Won't Work For

This strategy isn't for everyone:

If your career sees minimal income growth, the benefits diminish

If you're starting late (40+), you'll need a more aggressive approach

If you experience frequent income disruptions, you'll need more flexibility

Putting It Into Action

Start by figuring out your appropriate "reference salary":

Under 5 years in career: Use 70-80% of current salary

5-15 years in career: Use salary from 5 years ago

15+ years in career: Use salary from 7-10 years ago

Then, simply apply conventional budget percentages to that reference salary, not your current one.

The Bottom Line

Most financial advice presents a false choice: live for today OR save for tomorrow. The Time-Shifted Wealth Strategy rejects this premise by creating a third option—systematically delaying lifestyle inflation while still enjoying meaningful improvements.

By living like yesterday while earning like today, you create a wealth-building gap that compounds into the freedom to write your own financial future.

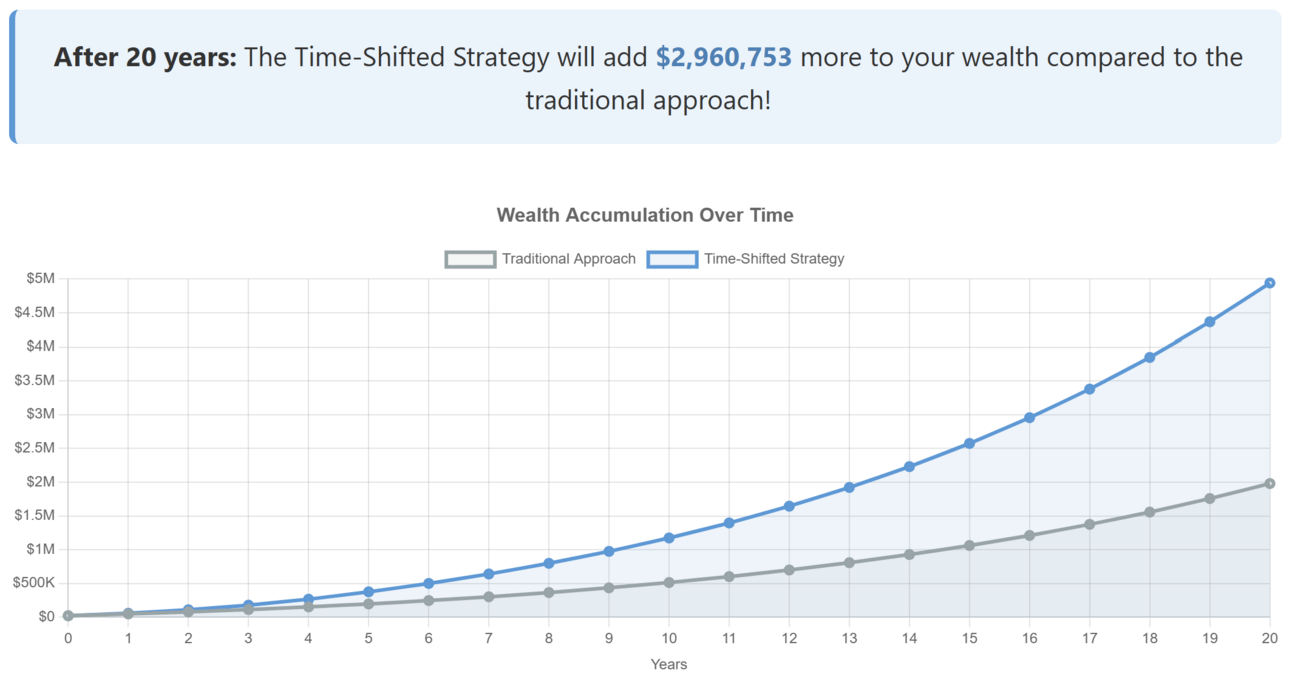

To calculate your own specific number for the time shifted wealth strategy check out my calculator linked here: Alex Kirkendall - Time Shifted Wealth Strategy

Here is an example of the output: